Our legislation updates make it easy for you to keep on top of the latest changes affecting your business. Receive our articles, opinions, tips, industry news, country profiles, regional overviews and studies, latest events and even more, directly into your mailbox.

We will send you only relevant information we consider may be of your interest and treat your personal data in compliance with our Privacy policy and GDPR statement.

The One Stop Shop or OSS in Poland procedure is an electronic one-stop shop for simplifying the settlement of output VAT on sales of goods and services to consumers from other EU countries, i.e. individuals who do not conduct business activities.

The premise of the OSS procedure in Poland is to enable settlement of VAT on the above transactions with the tax administration in one EU Member State. The taxpayer submits to one tax administration information on his sales of goods and services to individuals from other EU countries and pays the VAT. Based on the declarations submitted, the tax administration distributes and remits the appropriate part of the VAT paid in the country of identification to the relevant EU country of consumption.

The OSS procedure reduces the taxpayer’s obligations to register and settle VAT in different EU countries. Without OSS procedures, a supplier would generally be required to register in each Member State in which he sells goods or services to individuals.

There are two procedures available under the OSS procedure: the EU procedure and the non-EU procedure.

The EU procedure can be used, among others, by taxpayers established in the EU who:

supply services to natural persons in a Member State where they are not established, or

make intra-Community distance sales, i.e. a supply of goods made to individuals from other EU countries.

How to register for the OSS

Registration for the OSS procedure is made in a single Member State, the so-called Member State of Identification. In principle, the Member State of Identification is the Member State in which the taxpayer has its seat of economic activity.

The tax authority competent for the OSS procedure in Poland is the Head of the Second Tax Office Warsaw-Downtown.

To register for the OSS procedure, the following documents should be submitted:

VIU-R application in electronic form

Original PPS-1 power of attorney (if acting by proxy)

Confirmation in Form VIU-R that the address details are up to date and consent to receive letters electronically.

Registration for the OSS procedure will be effective for taxpayer from the first day of the calendar quarter following the quarter in which the VIU-R form was submitted.

What transactions should be reported in the OSS

Once registration to the OSS procedure is done, then VAT must be declared and settled on all supplies of goods or services covered by this procedure.

This means that after registration via the OSS procedure, output VAT will have to be reported on supplies of goods to individuals from other EU countries. It regards also supplies of below services to individuals from other EU countries:

accommodation services in hotels or and buildings with similar function;

cultural, artistic, sporting, scientific, educational, entertainment and similar services, such as trade fairs and exhibitions, as well as ancillary services to these services;

transport services;

services of valuation of and on movable tangible property;

services ancillary to transport services, such as loading, unloading, reloading and similar activities;

services connected with immovable property;

services for the rental of means of transport;

restaurant and catering services;

telecommunication, broadcasting and electronic services.

How to record transactions in the OSS

Once the OSS procedure has been notified, additional records of transactions covered by this procedure should be kept. These records are in electronic form and shall be kept for a period of 10 years from the end of the year in which the transaction took place.

These records should include the following data:

the Member State of consumption to which the goods or services are supplied;

the type of services or the description and quantity of goods supplied;

the date of the supply of the goods or services;

the taxable amount indicating the currency used;

any subsequent increase or reduction of the taxable amount;

the VAT rate applied;

the amount of VAT payable indicating the currency used;

the date and amount of payments received;

any payments on account received before the supply of the goods or services;

if an invoice is issued, the information contained on the invoice;

in respect of services, the information used to determine the place where the customer is established or has his permanent address or usually resides and, in respect of goods, the information used to determine the place where the dispatch or the transport of the goods to the customer begins and ends;

any proof of possible returns of goods, including the taxable amount and the VAT rate applied.

It should be emphasised that entities notified to the OSS are obliged to provide their records in electronic form whenever requested by the tax administration of both the Member State of identification and consumption.

How to report transactions in the OSS

VAT return (VIU-DO)

A taxpayer registered for the OSS procedure in Poland is required to submit via the e-Declaration system: VAT returns (VIU-DO).

The return shall be submitted on a quarterly basis by the end of the month following each consecutive quarter.

The table below shows the deadlines for submitting VAT returns (VIU-DO).

Settlement period – calendar quarter

Date of submission of return for OSS

Q1: 1 January do 31 March

30 April

Q2: 1 April do 30 June

31 July

Q3: 1 July do 30 September

31 October

Q4: 1 October do 31 December

31 January (next year)

Amounts on the VAT return shall be expressed in euro and shall not be rounded up or down.

The VAT return for the OSS is supplementary and does not replace the VAT return that the taxpayer submits in his Member State as part of his domestic VAT obligations.

This means that after registering for the OSS procedure, taxpayer will be obliged to submit, as before, JPK_VAT files (in which should be reported, for example, retail sales in Poland and distance sales from warehouses in Poland to Polish buyers), and in addition will submit VAT returns (VIU-DO) by the end of the month following each subsequent quarter.

A taxpayer using the OSS procedure shall submit a VAT return for each calendar quarter, irrespective of whether the supply of goods or services covered by the procedure has taken place.

This means that if there are no activities covered by the OSS procedure and no adjustments have been made relating to previous returns of the settlement period, a nil VAT return (VIU-DO) shall be submitted.

It should be underlined that the VAT return (VIU-DO) cannot be submitted before the end of the settlement period.

The deadline for submitting the return also expires if that day falls on a Saturday or a public holiday.

Adjustment of VAT return (VIU-DO)

Where mistakes are found in the VAT return (VIU-DO) submitted, the adjustment shall be made in the return submitted for the current tax period, but no later than 3 years after the expiry of the deadline for submission of the VAT return in which the mistakes were found.

The VAT return (VIU-DO) in which the correction is made shall indicate the Member State of consumption concerned, the tax period and the amount of VAT in respect of which the correction is made.

Nevertheless in the case of:

the expiry of three years from the deadline for submission of the original declaration,

discontinuation of the OSS procedure,

exclusion from the OSS procedure,

change of Member State of identification

– an adjustment of the VAT return (VIU-DO) shall be submitted electronically via a special IT application to the Łódź Tax Office.

Payment of the VAT amount in respect of which the adjustment is made should be done in euro to the bank account of the Łódź Tax Office.

How to pay VAT in the OSS

Once the VAT return (VIU-DO) has been submitted, it will be assigned a unique reference number (UNR).

The reference number (UNR) of the VAT return must always be indicated when making a payment. Without a reference number, it is not possible to make an effective payment and you should expect that such a payment will not be recognised and will be returned to the payer’s account.

The unique reference number for the EU procedure consists of the code of the Member State of identification, the VAT number and the period (quarter/year) for which the return is submitted.

An example of a UNR number for an EU OSS procedure is – PL/PLXXXXXXX/Q3.2023

The deadline for payment of VAT is the last day of the month following each consecutive quarter.

The deadline for submitting the return also expires if that day falls on a Saturday or a public holiday.

VAT resulting from the VAT return (VIU-DO) shall be paid in euro to the following bank account of the Second Tax Office Warsaw-Śródmieście:

84 1010 1010 0165 9315 1697 8000

PL84 1010 0165 9315 1697 8000 (BIC code: NBPLPLPW) – for payments from abroad.

The distribution of payments between the Member States of consumption is carried out by the tax authority on behalf of the taxpayer.

Example of how to complete the VAT return (VIU-DO)

The Taxpayer intends to apply for the OSS procedure and report in its VAT return (VIU-DO) the distance selling of goods to individuals from various EU countries.

To correctly complete the return for the above transactions, it is necessary:

in section C2 report deliveries of goods from warehouses in Poland to buyers from other EU countries;

in section C3 to report deliveries of goods from warehouses in EU countries other than Poland to buyers from EU countries other than the country of dispatch.

In addition in section C.5. adjustments to the VAT amounts indicated in the returns for previous periods resulting from corrections to supplies of goods or services (no later than 3 years after the deadline for submission of the original return) should be reported.

In section C.6. the balance of output tax should be reported for each Member State of consumption. This position is filled in automatically and is the sum of the VAT amounts from Sections C.2, C.3, C.4 and C.5 for the Member States of consumption indicated. It should be noted that the value of the amount of output VAT for specific Member State of consumption can be in negative (in the case of adjustments in minus).

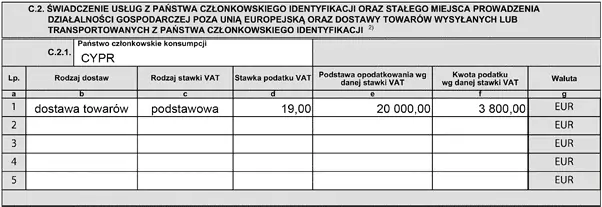

Section C2 – deliveries of goods from Poland to buyers from other EU countries

This section should report supplies of goods from warehouses in Poland to buyers from other EU countries. In each part of this section, the values of total sales in the given settlement period to a specific EU country should be reported.

Individual items should be completed as follow:

Member State of consumption – indicate the name of the Member State of consumption on whose territory the supply of services and goods took place during the relevant settlement period.

Type of supply – indicate whether it concerns a supply of services or a supply of goods dispatched or transported.

Type of VAT rate – indicate the appropriate type of VAT rate – standard or reduced.

VAT rate – indicate the rate applicable to the Member State of consumption.

Taxable amount for a given VAT rate – provide the taxable amount for the rate (standard, reduced) indicated in the field “VAT rate type”.

Amount of VAT at given VAT rate – enter the amount of tax at the rate (standard, reduced) for the Member State of consumption concerned. The amount expressed should be given in euro.

Example:

A taxpayer registered for the EU procedure in Poland has made supplies of goods to Cyprus in the third quarter of 2025 for €20,000 (VAT rate 19%).

The supply transactions to this country should be reported in the VAT return (VIU-DO) as follows:

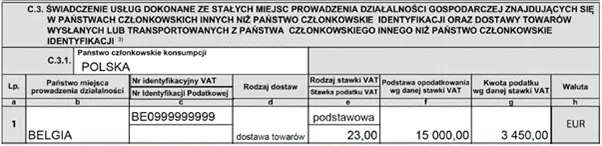

Section C3 – deliveries of goods from EU countries other than Poland to buyers from EU countries other than the country of dispatch

This section should report deliveries of goods from warehouses in countries other than Poland to buyers in EU countries other than the country of dispatch. In each part of this section, the values of total sales in the given settlement period to a specific EU country should be reported.

Individual items should be completed as follows:

Member State of consumption – indicate the name of the relevant Member State of consumption on the territory of which services were provided and goods were supplied during the settlement period.

Country of establishment – indicate the name of the country where the fixed establishment, other than the Member State of identification, from the territory of which the supply of services or goods took place, is located.

VAT identification number – indicate the domestic VAT identification number that was provided in the registration declaration (field 20. in section B.4 in VIU-R (3)), where the taxpayer has a fixed establishment outside the Member State of identification.

Tax identification number – indicate the tax identification number that was provided in the registration declaration (field 21. in section B.4 in VIU-R (3)), in case there is no VAT identification number.

Type of supply – indicate whether it concerns the supply of services or the supply of goods dispatched or transported.

Type of VAT rate – indicate the appropriate type of VAT rate – standard or reduced.

VAT rate – indicate the rate applicable to the Member State of consumption.

Taxable amount for a given VAT rate – provide the taxable amount for the rate (standard, reduced) indicated in the field “VAT rate type”.

Amount of VAT at given VAT rate – indicate the amount of tax at the rate (standard, reduced) for the Member State of consumption concerned. The amount expressed should be given in euro.

Example:

A taxpayer registered for the EU procedure in Poland made supplies of goods from a warehouse in Belgium to Poland in the third quarter of 2025 for €15,000 (VAT rate 23%).

The supply transactions to this country should be reported in the VAT return (VIU-DO) as follows:

In general, Polish citizens, as well as Polish companies can purchase and sell real estates. Similar rules apply to citizens and companies from EU and EEA member states.

During the procedure of accession to European Union, Poland negotiated 12-year grace period of protection with regard to agricultural parcels. During this period EU residents were obliged to obtain a permit to purchase agricultural parcels. This protection period has ended in May 2016.

Nevertheless, there are still some restrictions concerning acquisition of the agricultural parcels. They apply to all potential purchasers, regardless the nationality.

Sale of agricultural parcels which are the state property has been suspended until April 30th, 2026. There are also restrictions concerning sale of agricultural parcels owned by private persons. Detailed rules of acquisition of agricultural parcels are presented below.

General information about real estate transfer process

The ownership of the real estate may be transferred by conclusion of several types of agreement, e.g.:

purchase

exchange

donation agreement

The agreement obliging to transfer the ownership of real estate must be executed in the form of notarial deed. The ownership of a real estate cannot be transferred conditionally or with a reservation of a time limit.

The common practice is to conclude preliminary agreement prior to conclusion of the main agreement. Legal consequences of such agreement will differ depending on its content and the form in which it was concluded. If preliminary agreement was concluded in form required for the main agreement (in this case notarial deed) entitled party may pursue conclusion of the agreement in court even if the other party refuses to fulfil its obligation. However, if preliminary agreement does not fulfil formal requirements, entitled party may only demand payment of compensation for the damage caused by the lack of conclusion of the agreement.

The ownership of the real estate may be also acquired by so-called usucapion (acquisitive prescription). In the event of adverse possession of a real estate (i.e. occupation without legal title), possessor of real estate acquires ownership of this real estate after specified period. The period depends on good faith of the possessor and amounts to 20 years – in case of good faith – or 30 years – in case of bad faith – of uninterrupted possession of the real estate.

Usual scenario of the real estate transactions and fees

Due diligence

The majority of real estate in Poland are disclosed in land and mortgage registers. The registers are held by district courts and are public. They may be viewed free of charge on the website of Ministry of Justice.

Prior to conclusion of the agreement the purchaser should verify the legal condition of real estate he/she intends to buy in land and mortgage register. To check the real estate’s register the purchaser will need its registry number. The purchaser should in particular check the information about the owners of the real estate and any possible rights of third persons in relation to the real estate, e.g.: mortgage.

Polish law guarantees the authenticity of the information disclosed in the land and mortgage register. It means that in case of acquisition of the ownership or other right ad rem to a real estate from the person disclosed in land and mortgage register as the owner, the acquisition is valid even if this person was not in fact the owner of the real estate. However, such protection does not apply to the purchaser who knew about the inconsistency of the register or could have easily learnt about such inconsistency.

If the real estate is not registered in land and mortgage register, the purchaser should check land and building records. These records do not contain information as detailed as the land and mortgage register. Nevertheless, they include all basic information, such as real estate’s owners, their addresses of residence or seats, cadastral value of the property etc.

Conclusion of the agreement

The agreement which transfers the ownership of a real estate has to be executed in the form of notarial deed or else it will be invalid.

Notary fee for preparation of a notarial deed depends on the value of sold real estate. However, the fee cannot exceed PLN 10,000.

The notary will also calculate due civil law transaction tax. The tax is paid to the notary at the conclusion of the agreement. The notary is obliged to transfer it to the relevant tax office.

Obligations after the purchase

After the conclusion of the agreement the purchaser of the real estate should file a motion for update information disclosed in land and mortgage register. The motion should be filed in the relevant district court. The court fee amounts to PLN 200. There is also a possibility to ask the notary to do it for us.

In the event of lack of land and mortgage register, the purchaser may establish such register for the purchased real estate. This also requires a motion to the district court with jurisdiction over the location of the property. The court fee in such case amounts to PLN 60.

The purchaser of real estate should also inform relevant municipal office about the change of the owner of the real estate in order to provide information about new payer of the property tax.

Limitations over the acquisition of the real estate

Acquisition of real estates by foreigners

Acquisition of real estate in Poland by foreigners is regulated by the Act on Acquisition of Real Estate by Foreigners dated March 24th, 1920 (Official Journal from 2017, position 2278).

According to this Act the foreigner is:

natural person not having Polish citizenship;

legal person having its seat abroad;

company without legal personality having its seat abroad, established by persons referred in point 1 and 2 in compliance with statutory law of foreign state;

legal person (or company without legal personality) having its seat in Poland, which is directly or indirectly controlled by persons indicated above.

Under the Act acquisition of perpetual usufruct requires fulfilment of the same conditions as acquisition of ownership.

The acquisition of real estate by a foreigner requires a permit. The permit is issued by the Minister of Internal Affairs. The Minister of National Defence or the minister competent for rural development (in case of agricultural parcels) have a right to oppose such acquisition.

The permit is issued upon the foreigner’s request if:

the acquisition of real estate does not threaten the defense or security of the state or the public order, as well as if the interest of social policy and public health do not oppose to such acquisition;

foreigner proves that there are circumstances which confirm his/her ties with the Republic of Poland (e.g. Polish nationality, marriage with Polish citizen, doing business in Poland in accordance with Polish law etc.).

Permit is also required in case of acquisition of shares in a company with its seat in Poland by foreigners, as well as any other legal action concerning shares of the company, if:

in the result of such action the company which is an owner or a perpetual usufructuary of real estate in Poland will become a controlled company or

if the company which shares are acquired is a controlled company and the shares are acquired by a foreigner who is not a shareholder of this company.

Acquisition of a real estate which violates the provisions of the Act on Acquisition of Real Estate by Foreigners is null and void.

Most of the limitations do not apply to residents of member states of European Union, European Economic Area and Swiss Confederation.

Acquisition of agricultural parcels

In general acquisition of agricultural parcel is reserved for so-called “individual farmers”.

Individual farmer is a term introduced by the Act on Shaping the Agricultural System dated April 11th, 2003 (Official Journal from 2022, position 2569) and means a natural person, who:

is the owner, perpetual usufructuary, autonomous possessor or tenant of agricultural land of total utilised agricultural area not exceeding 300 hectares,

possess agricultural qualifications (i.e. is educated in agriculture or has appropriate work experience in agriculture),

is residing in the municipality, on the territory of which the agricultural parcels are located for at least 5 years;

personally runs the farm for all the time stated above.

The acquisition of the agricultural parcels by persons who are not individual farmers is possible in particular in the following cases:

the purchaser is close relative of the vendor (which means descendants, ascendants, siblings, sibling’s children, siblings of parents, spouse, parents-in-law, adopters and adopted individuals, stepchildren, stepparents, and stepchildren)

the purchaser is a commercial company:

of which the sole shareholder or shareholder is the State Treasury, being the operator of the transmission system or holding a concession for the transmission of liquid fuels, within the meaning of the Act of April 10, 1997 – Energy Law

which is the operator of the gas distribution system within the meaning of the Act of April 10, 1997 – Energy Law, in the case of acquiring agricultural real estate for purposes related to the construction, modernization, or expansion of the gas distribution system

a capital company or capital group, as referred to in Article 1(1) of the Act of March 18, 2010, on special powers of the minister responsible for state assets and their exercise in certain capital companies or capital groups operating in the sectors of electric energy, crude oil, and gaseous fuels (Journal of Laws of 2020, item 2173), is entitled to acquire agricultural real estate for purposes related to the construction, modernization, or expansion of the infrastructure in the sectors of electric energy, crude oil, and gaseous fuels

the purchaser is an entity of local self-government or the State Treasury

the purchaser is a church or religious association

the purchaser is a national park – in case if the acquisition of agricultural parcel is associated with nature conservation

the purchaser is agricultural production cooperative

the entity that has sold agricultural real estate for purposes related to the construction of a marine wind farm within the meaning of Article 3(3) of the Act of December 17, 2020, on promoting the generation of electric energy in marine wind along with a set of devices for power extraction within the meaning of Article 3(13) of this Act, or has been expropriated for purposes specified in this Act – if acquiring agricultural real estate with an area not exceeding 150% of the area of the sold agricultural real estate within 3 years from the date of the sales agreement or within 3 years from the date when the decision on expropriation of the agricultural real estate became final

the purchaser is a person who has sold agricultural real estate for purposes related to the implementation of an investment in the construction of a nuclear power facility or an associated investment within the meaning of the provisions of the Act of June 29, 2011, on the preparation and implementation of investments in the field of nuclear power facilities and associated investments, or has been expropriated for purposes specified in this Act – if acquiring agricultural real estate with an area not exceeding 150% of the area of the sold agricultural real estate within 3 years from the date of the sales agreement or within 3 years from the date when the decision on expropriation of the agricultural real estate became final

the purchaser is Investor as referred to in Article 3a(2) of the Act of June 29, 2011, on the preparation and implementation of investments in the field of nuclear power facilities and associated investments

agricultural real estate has an area smaller than 1 hectare

inheritance of a real estate

acquisition of a real estate on basis of article 151 and article 231 of Civil Code

acquisition of a real estate in the course of restructuring proceeding

during enforcement and bankruptcy proceedings

as a result of abolishing co-ownership, division of marital property after the termination of marriage, and estate distribution;

as a result of the division or merger of commercial companies

as a result of the transformation of an entrepreneur or civil partnership into a commercial company based on the provisions of the Act of September 15, 2000 – Commercial Companies Code.

The acquisition of agricultural real estate by entities other than those mentioned above may also occur with the consent of the Director-General of the National Center, expressed through an administrative decision issued upon request, but only in specific cases defined by regulations.

Obligations of a purchaser of agricultural parcels

The purchaser of the agricultural parcel is obliged to run the farm, which was a part of acquired agricultural parcel for at least 10 years from the date of acquisition. If the purchaser is a natural person – he/she is obliged to fulfil this requirement personally.

During this 10-year period the acquired agricultural parcel cannot be sold or given into the possession of other person.

Priority right

The tenant of agricultural parcel, who fulfils requirements specified in the Act on Shaping the Agricultural System, has a priority in purchasing it. If there is no tenant entitled to priority right or if he/she does not exercise this right, the priority in purchasing the agricultural parcel is passed to the State Treasury.

The above rules do not apply if:

the purchaser is a person close to the vendor, an entity of local self-government or the State Treasury;

relevant authorities granted a purchaser a permission to acquire the agricultural parcel;

the sale is concluded between legal entities of the same church or religious association.

Exclusion of the application of the provisions of the Act on Shaping the Agricultural System

The requirements regarding the transaction of agricultural real estate introduced by the Act on Shaping the Agricultural System do not apply when the arable land area in the sold real estate is a maximum of 0.2999 hectares.

Real estate transfer taxation

As mentioned above, real estate can be sold either through a direct sale of the property (an asset deal or enterprise deal) or indirectly through sale of shares in the company owning the property (a share deal). These three types of transactions have different tax implications under the Polish tax regulations.

Asset deal

The revenues derived from the sale of real estate are subject to the standard taxation rules of Polish corporate income tax. Taxable revenues are reduced by the net book value of the property. Thus, effectively, only the “capital gain” is taxed at the rate of 19%. If the sales price differs substantially and without a justified reason from the market value of the real estate, the revenue may be assessed by the tax authorities according to the market value. This price adjustment may be applied to transactions between related and unrelated entities.

Costs incurred by the buyer for the acquisition of real estate: purchase price, transaction costs including advisory, civil law transaction tax – if applicable, financial costs accrued till the purchase, etc., are to be allocated to the initial value of the real estate and are recognized as tax deductible costs through depreciation write-offs or upon sale. As the value of the land is not subject to depreciation.

VAT on the sale of real estate

The supply of buildings, infrastructure, or parts of buildings or infrastructure is generally VAT exempt, except for:

the supply of a building, infrastructure or part of a building or infrastructure in the course of its first occupation or prior to it; and

the supply of a building, infrastructure or part of a building or infrastructure made within two years of the first occupation;

in which cases the supply of buildings, infrastructure or parts of buildings or infrastructure are generally subject to VAT.

“First occupation” is understood as handing over a building, infrastructure or part of a building or infrastructure within the context of the performance of VAT-able activities (subject to VAT or VAT exempt) to the first acquirer or user, after the:

initial completion; or

improvement (if the expenses incurred for the improvement constituted at least 30% of the initial value).

of that building, infrastructure or part of a building or infrastructure.

Taxpayers may choose not to apply the exemption and charge VAT if:

buyer and seller are VAT registered; and

before the day of supply they submit the appropriate joint statement to the tax office of the purchaser or include relevant statement in sales agreement.

The supply of buildings, infrastructure or parts of buildings or infrastructure which should be subject to VAT (i.e. supply in the course of first occupation or within two years of the first occupation) must be VAT exempt (no option to tax allowed) if:

the seller was not entitled to deduct input VAT; and

the seller did not incur improvement expenses on which he had right to deduct VAT, or such expenses did not exceed 30% of the initial value of the building, infrastructure or part of a building or infrastructure.

The VAT treatment of transfer of land or perpetual usufruct (RPU) over in general the VAT treatment of the buildings developed on the land.

However, if an RPU is acquired for the first time from the State or local authority, the transfer is always subject to 23% VAT, even though the buildings developed on the land may be exempt from VAT.

The supply of ownership title / RPU to undeveloped land qualified as land for development purposes is subject to 23% VAT (supply of agricultural land exempt from VAT).

Supply of residential buildings and separate apartments is subject to a reduced 8% VAT, except for part of residential buildings whose usable floor space exceeds 300 m2 and apartments whose usable floor space exceeds 150 m2. In such a case the part exceeding the thresholds is subject to a 23% VAT rate.

TCLT

If the supply of real estate is VAT exempt, it is subject to civil law transaction tax payable by the buyer. The applicable rate is 2% of the market value of the real estate. This tax is levied on the total value of the building, infrastructure, or parts thereof, and the land / RPU.

Recoverability of input VAT by the buyer

Input VAT is recoverable if the company performs or intends to perform activities in the future which are subject to VAT (e.g. lease of the commercial real estate). Input VAT will not be recoverable if the company performs or intends to perform activities in the future which are VAT exempt. If this is the case, the input VAT will increase the initial tax basis of the real estate.

If business activities are partly exempt, any input VAT which cannot be matched directly either to VAT-able sales or VAT exempt sales may be recovered according to the proportion of the net value of the taxed supplies to the total value of all supplies (a so called pro rata recovery). During a calendar year, the proportion is calculated based on the volume of supplies made in the previous year. At the year end, the amount of deductions is adjusted to the actual percentage calculated for the whole year. In the case of real estate subject to depreciation for tax purposes, the percentage of input VAT which may be deducted is subject to adjustments over the period of 10 years. Taxpayers also need to take into account so called preliminary pro-rata that limits input VAT recovery on purchases, if linked both with the business of the taxpayer and other activities not related with business operations.

Declaring input VAT for recovery

The right to recover input VAT arises in the period when the tax point with respect to the acquired goods or services arose (i.e. in the month in which the services were rendered, or the goods were acquired by the purchaser). It cannot be, however, recovered earlier than in the period in which the taxpayer receives the respective invoice (prepayment invoices do not fall under this rule: they must be paid in order for input VAT to be reclaimable).

Direct refund of input VAT

A direct refund of any surplus input VAT should be made within 60 days of the submission of the application for the refund provided that in the period for which the refund is claimed the taxpayer performed VAT-able supply.

This deadline can be shortened to 25 days at a taxpayer’s request when a number of conditions are met, such as providing bank payment proofs for invoices, invoices paid in cash amount to less than PLN 15,000 in total.

In the case where VAT-able supplies are not made in the period for which the refund is claimed. The period for the refund is extended to 180 days, unless a form of security is provided (in which case the refund must be made within 60 days).

Enterprise deal

The revenues derived from the sale of an enterprise are subject to the standard taxation rules of Polish corporate income tax. Thus, effectively, only the “capital gain” is taxed at the rate of 19%.

Verification of status of enterprise deal or organized part hereof

Enterprise is an organized complex of material and non-material components designed for carrying on an economic activity.

Organized part of an enterprise are material and non-material components organizationally and financially separated in an existing enterprise, including liabilities, being designed for the fulfilment of specific economic tasks, which at the same time could constitute an independent enterprise carrying out these tasks on its own..

According to clarifications of the Ministry of Finance on VAT consequences upon sale of commercial real estates, if beside typical items sold together with a real estate, rights and obligations from debt financing agreements, property management agreement, asset management agreement and agreements on financial nature are transferred as well as the intention of the purchaser is to continue the business activity of the seller and such continuation is possible via purchased items such sale will constitute an enterprise deal transaction.

VAT on the sale of enterprise or organized part of hereof

Sale of the enterprise or organized part of an enterprise is out of VAT scope.

TCLT

Purchase of enterprise or organized part of the enterprise is subject to civil law transaction tax payable by the buyer. The applicable rate is 2% of the market value of the real estate, movables, etc. Other property rights may be subject to 1% TCLT rate (if separated in the sales agreement).

Share deal

A capital gain on the sale of shares is subject to Polish corporate income tax at the standard rate of 19%.

If the selling party is a foreign shareholder, the applicable tax treaty influences the tax implications of such a transaction.

Significant part of Polish tax treaties (e.g. with Spain, France, Denmark, Sweden, Germany, Luxembourg) provide that a sale of shares in a company holding mainly real estate assets should be regarded as a sale of real estate. Consequently, income earned on the sale of shares in the Polish company will be taxed in Poland (the so called real estate clause).

The sale of shares in the Polish company is subject to a 1% civil law transaction tax (on the fair market value of shares) payable by the buyer. This is irrespective of where the transaction takes place or where the parties to the transaction are tax residents. A share transaction is not subject to Polish VAT. However, where a share transaction is treated as being made in the course of business activity (rather than as a one– off transaction), it may be classified as a VAT exempt financial service. However, it will still be subject to civil law transaction tax.

Costs which must be incurred in order to acquire shares (e.g. purchase price and notary fees) may be recognized as tax deductible costs upon the sale of shares.

Other costs indirectly connected with acquisition of shares such as financing costs may be recognized as tax deductible costs when incurred (in certain cases recognition over time may occur).

Comprehensive support for real estate transactions in Poland

Handling real estate transactions in Poland requires not only legal precision but also deep knowledge of local procedures and regulations. Our Polish experts offer end-to-end support, from legal due diligence and contract drafting to tax advisory and compliance, ensuring your property deals are secure, efficient, and fully compliant. Whether you’re buying, selling, or investing, we help you navigate every step with confidence.

While in the realm of transfer pricing in Poland, the year 2025 will not bring groundbreaking changes, taxpayers will still be required to adhere to the existing regulations concerning the documentation and reporting of transactions. Increased scrutiny and growing interest from tax authorities in this area demand particular attention and precision in documentation from entrepreneurs. Business owners must be prepared to meticulously document transactions with related entities to avoid potential issues during tax inspections. This is particularly crucial in the context of international business operations, where transfer prices may be a subject of heightened interest for tax authorities.

Below we present the key information in the area of transfer pricing in Poland.

Transactions subject to transfer pricing documentation

Entities shall be deemed to be related entities where, directly or indirectly, significant influence is exerted.

Significant influence according to the CIT Act means:

Direct or indirect holding of at least 25%:

shares in the capital

voting rights in the company

shares or rights to share in profits or assets or their benefits.

The natural person’s actual ability to influence key economic decisions of the legal person or a flawed legal person

Marriage or kinship or affinity to the second degree

Entities deemed as related are required to prepare transfer pricing documentation if the volume of individual transaction exceeds the value:

10 000 000 PLN – in case of goods transaction

10 000 000 PLN – in case of financial transaction

2 000 000 PLN – in case of service transaction

2 000 000 PLN – in case of other transactions

Regardless of the prerequisites for the existence of relationships between entities, transfer pricing regulations may be applied to transactions, agreements or undertakings with entities from tax havens:

exceeding PLN 2 500 000 – in case of financial transaction

exceeding PLN 500 000 – in case of transactions other than financial

Scope of transfer pricing documentation

The three-level concept

The general concept of the transfer pricing documentation has been maintained. The three levels of reporting consist of:

Local file + benchmarking study

Master file

Country by Country reporting

Local file + Benchmarking

Represents local documentation containing details of transactions or other events between the Polish company and other group companies disclosed in the accounting books.

The taxpayer is obliged to prepare transfer pricing documentation in the case of perform a controlled transaction with a related entity, if its value exceeds the threshold indicated in the Act.*

The local file shall include in particular:

Description of the taxpayer including description of the management structure and organisation chart

Description of the main activities of the taxpayer

Description of the transaction, including analysis of the functions, risks and assets

Information about related entities (parties to the transaction)

Transfer price calculation method

Benchmarking analysis or compatibility analysis (obligatory part under the new regulations)

Financial data

Description of any agreements or tax interpretations related to the transaction (including Advance Pricing Agreements)

The source documents (i.e. contracts).

Description of any agreements or tax interpretations related to the transaction (including Advance Pricing Agreements)

The source documents (i.e. contracts).

*PLN 2/10 millions

Benchmarking study is an analysis of the settlements between unrelated entities in transactions all over the market deemed as comparable to conditions established in controlled transactions. Benchmarking study is usually prepared based on specialized databases and market reports.

Comparability analysis’ goal is to prove that the terms and conditions under which the controlled transaction was executed comply with those which would have been determined by unrelated parties (transaction complies with arm’s length principle).

Entities obliged to prepare a TP documentation (local file + benchmarking study) are required to submit the statement that:

The documentation has been prepared

The prices applied to the controlled transactions are arm’s length.

Under the changes effective January 1st, 2022, the statement is included in the TPR return.

The taxpayers who execute both transactions subject to the documentation obligation and transactions exempted under Art. 11n (1) of Polish CIT Law are obliged to submit TP-R report.

Master file

Master file should be prepared by taxpayers:

Obliged to prepare TP documentation

Members of a group of companies that consolidate the financial data with a full or proportional method, if the consolidated group revenues exceed PLN 200 000 000.

The master file shall include the following:

Description of the entity preparing the documentation including the organizational structure

The Transfer Pricing policy

Description of the group’s business activity

The group’s financial situation

Detailed information on intellectual property (including especially the group strategy on creation, development and maintenance of intellectual property)

Description of any agreements concerning income taxes made between the group components and the tax authorities in other countries (including unilateral APAs).

TPR

The TPR return requires the taxpayers to provide a detailed overview of transfer pricing surrounding, including the financial indicators, ratios and information of a given entity based on financial statements.

TPR is an obligatory part for entities which conclude controlled related party transactions fulfilling the criteria for transfer pricing documentation (simply, as a rule: if you are obliged to prepare Local File – then you have to submit TPR), as well as (in a limited scope) entities qualifying for the so-called domestic exemption under which they are not obliged to prepare transfer pricing documentation.

Country-by-country reporting (CbCR) and notification (CbCP)

The report on the global allocation of income and tax within the group (required for groups where the parent company consolidating the accounts is located in Poland) must be filed by the holding company if the consolidated revenues of the group exceed EUR 750 million.

The CBC-P notification is required to be submitted by each entity in the group to which the CbCR obligations apply. The CBC-P notification can only be submitted electronically, with the deadline set for 3 months following the end of the tax year.

Exceptions for documentation in transfer pricing in Poland

According to the current regulations, the following categories of transactions are not subject to Transfer Pricing documentation:

Concluded by related parties having their registered office, place of residence, seat or management on the territory of the Republic of Poland, as long as they:

do not benefit from tax exemption under the Act on Special Economic Zones

do not benefit from a CIT exemption

do not benefit from the tax exemption on the basis of the Act on Support for New Investments

have not incurred a tax loss.

Concluded between foreign fixed establishments of related entities located in the territory of the Republic of Poland, having their place of residence, registered office or management board in the territory of a Member State of the European Union or another state belonging to the European Economic Area other than the Republic of Poland

Concluded by a foreign fixed establishment, located in the territory of the Republic of Poland, of an entity having its place of residence, seat or management board in the territory of a European Union member state or another state belonging to the European Economic Area, other than the Republic of Poland, with an affiliated entity having its place of residence, seat or management board in the territory of the Republic of Poland

For which APA has been concluded

Whose value does not constitute revenue or tax-deductible cost on a permanent basis (exceptions – financial transactions, capital transactions, investment, fixed assets or intangible assets transactions)

If the relationship results only from a connection with the State Treasury or local government units

In which the price was determined by means of an open tender on the basis of the Public Procurement Law

Consisting of the attribution of income to a foreign permanent establishment situated in the territory of the Republic of Poland by non-residents, if the regulations of relevant international agreements to which the Republic of Poland is a party provide that such income may be taxed only in a State other than the Republic of Poland

Between companies forming a tax group

Consisting only in making a settlement between related parties of expenses incurred for the benefit of an unrelated party, as long as they,

no added value is created and the settlement is made without taking into account the margin or profit mark-up

the settlement is not directly related to another controlled transaction

settlement occurred immediately upon payment to an unrelated party

the related party is not an entity that has its place of residence, registered office or management in a territory or country applying harmful tax competition

Constituting low added-value services – if the conditions set forth in art. 11f of Polish CIT Law are met or

Concerning a loan, credit or bond issue – if the conditions specified in art.11g of Polish CIT Law are met.

Transfer pricing methods

Generally, the transfer pricing methods accepted by the tax authorities are based on the OECD Guidelines. These methods are:

CUP (Comparable Uncontrolled Price Method)

Resale Price Method

Cost Plus

TNMM (Transactional Net Margin Method)

Profit Split Method

When selecting a price calculation method, taxpayer should make sure it is appropriate for the transaction. Since 2019, there is no obligation to use traditional methods before profit-sharing methods.

The new regulations also allow for the use of another method, including a valuation technique, if none of the five above methods can be used.

Safe harbours

Since 1st January 2019, the so-called Safe Harbour provisions have been introduced into Polish transfer pricing regulations. Safe Harbour ensures that certain transactions executed by taxpayers will not be subject to adjustment, provided they meet the conditions specified by the legislator.

These transactions are:

Low added-value services

Loan (credit and bond) agreements.

Safe harbour for low value-added services could be applied where the cost mark-up for these services has been determined on the basis of the cost plus or TNMM method and is equal to:

No more than 5% of the costs in case of purchase of services

Not less than 5% of the costs for the provision of services

Moreover, the service provider must not have its place of residence, registered office, or management in a tax haven. The recipient of the service should also possess a detailed service price calculation, which includes the type and amount of costs incurred, the method of allocation, the justification for the selection of allocation keys for all related parties using the services, and a description of the transaction, including an analysis of functions, risks, and assets.

In contrast, the conditions for applying the Safe Harbour provisions to loans require that the interest rate be determined based on the type of base interest rate and margin specified in the Minister of Finance’s notice. Additionally, the loan agreement must not include any provisions for remuneration other than interest payable to the lender, and the loan must not have a term exceeding five years.

The Ministry of Finance has decided that from January 1, 2025, for the purposes of safe harbour regulations for loan, credit and bond issues, the margin will be changed so that the maximum margin for borrowers will be 2,60 percentage points, while leaving the minimum margin for lenders at the current level of 2.00 percentage points.

It is important to note that, to benefit from the protection offered by the Safe Harbour provisions for loan transactions, the total level of liabilities or receivables of the company with related parties must not exceed PLN 20,000,000 or its equivalent in another currency. Additionally, the lender must not have its residence, registered office, or management located in a tax haven.

Deadlines

The regulations in force since 1st January 2022 have significantly modified the deadlines for the obligation to submit the TPR and to prepare the documentation itself. These obligations must be fulfilled until:

the end of the 10th month following the end of the tax year – preparation of TP documentation

the end of the 11th month after the end of the tax year (with the same rule – for transactions occurred in 2024 and next years) – submission of TPR return.

A separate TP statement will no longer be required.

In case of benchmarking study, the analysis should be updated at least once every 3 years (if the business circumstances change in a way affecting the analysis the benchmarking analysis should be reviewed earlier).

Moreover, according to the present regulations, the tax authorities may request the taxpayer to prepare documentation in respect of transactions / events even if the value does not exceed the limits, provided that the circumstances suggest that their value could have been underreported in order to avoid the documentation obligation. In that case, Transfer Pricing documentation should be submitted within 30 days of the request. This obligation does not apply to micro-entrepreneurs.

For the “standard” TP obligations (after exceeding the thresholds) taxpayers are obliged to present complete TP documentation within 14 days of the tax authorities’ request (previously : within 7 days).

Country-by-country reporting

The Country by Country reporting obligation applies to:

Polish entities, which simultaneously:

are the ultimate (dominating) entities in their groups

are the entities consolidating financial reports

operate directly or indirectly outside of Poland

their last year’s consolidated income within and outside of Poland is over the equivalent of EUR 750 Mio.

Entities not being the ultimate parent if there is no other entity designated to provide such information in the group if one of the following criteria are met:

the ultimate parent entity is not obliged to file a CbCR for the reporting year in its tax jurisdiction

the appropriate jurisdiction in which ultimate parent entity is resident for tax purposes has not undertaken to share information about the entity group within 12 months of the end of the given reporting year

the tax jurisdiction of the ultimate parent entity suspended automatic sharing of CbCR or failed to fulfil the obligation without notifying the dominating entity.

According to the present tax regulations members of groups of entities will be obliged to:

notify that they are the ultimate parent entity or designated entity (or a different entity obliged to file the CbCR), or

indicate the entity obliged to file CbCR together with its identity and tax residence.

The notification should be filed up to 3 months following the end of the reporting financial year of a group of entities. The new regulation* indicates what information should be included in the information about a group of entities.

The tax regulations provide fines for failure to fulfil these obligations (maximum amount: PLN 1 mln).

*The Regulation of the Minister of Finance of 13 June 2017 on the detailed scope of data to be included in the information about a group of entities.

Advance Pricing Agreements

Currently, the Advanced Pricing Agreement (APA) is issued at the discretion of the Head of the National Fiscal Administration (KAS). It serves as a confirmation of the selection and application of a method for determining transaction prices between related parties.

The primary advantage of obtaining such a decision is the elimination of the risk of transfer pricing methodology being challenged, provided the taxpayer adheres to the APA provisions. It also offers protection from penal and fiscal sanctions for individuals responsible for tax settlements.

An additional benefit of an APA was the ability to recognize certain costs, such as low-value-adding services, as deductible under the limitations of Article 15e of the Polish CIT Law. However, since 2022, Article 15e has been repealed, significantly reducing the advantages associated with APAs.

Some further rules regarding APA are as follows:

The possibility of applying for an APA by a foreign investor considering doing business in Poland by establishing a subsidiary company

The APA is valid from the beginning of the tax year in which the application has been submitted

Clarification of the elements of the application – following the model of local transfer pricing documentation

Applying for APA covering transactions under proceedings or tax control during one of the last two tax years preceding the tax year in which the application is made is no more possible.

The fee is 1% of the value of the transaction covered by the APA limited by the following:

For a unilateral APA referring to domestic entities only – min. fee: PLN 5 000 (approx. EUR 1170) and max. fee PLN 50 000 (approx. EUR 11 700) An APA referring to a foreign entity – min. PLN 20 000 (approx. EUR 4 680) and max. PLN 100 000 (EUR 23 400) A bilateral or multilateral APA – min. PLN 50 000 (approx. EUR 11 700) and max. PLN 200 000 (approx. EUR 46 800).

Renewal fees are half of the amount of the fee for the renewed APA.

*1 EUR = 4.2730 PLN (ex. rate 31/12/2024)

Recharacterizations and disregard of transaction

Since 1 January 2019, new mechanisms have been introduced into Polish tax legislation, enabling tax authorities to estimate revenue more effectively. These mechanisms include:

Recharacterization of a transaction

Disregarding of a transaction

The tax authorities may apply recharacterization or disregarding of a transaction if, in comparable circumstances, unrelated parties acting with economic rationality would not have entered into the controlled transaction in question.

When assessing such cases, the tax authorities consider the conditions agreed upon between related parties and whether those conditions prevent the transfer price from being set at a level that would have been agreed upon by economically unrelated parties, based on realistically available options.

The potential effects of these mechanisms are as follows:

Disregarding a transaction: The tax authorities assess the income or loss of the taxpayer without taking the controlled transaction into account.

Recharacterization: The tax authorities assess the income or loss of the taxpayer based on the transaction that would have been conducted by unrelated entities under similar circumstances.

However, tax authorities are prohibited from using these tools solely due to:

Difficulties in verifying the transfer price.

The absence of comparable transactions between unrelated parties in similar circumstances.

Transfer pricing adjustments

To meet the taxpayers’ expectations, the legislator pointed out that a taxpayer can recognize a transfer pricing adjustment by changing the amount of revenues or expenses if the following cumulative conditions are met:

Controlled transaction was performed at arm’s length

There was a change in significant circumstances affecting the terms of transaction or costs/revenues influencing the transfer pricing became known and the prices must be adjusted to comply with market terms

The taxpayer has a statement from the related party that if has adjusted the transfer prices in the same way. Beginning in 2022, it was allowed to have a statement or accounting proof from the related party.

The related party has its place of business in Poland or in a country or territory with which Poland has an agreement to avoid double taxation and there is a legal basis for exchanging tax information with that country

Cooperation agreements

The cooperation agreements have been introduced to the Polish tax system due to the Act on Resolving Double Taxation Disputes and Concluding of Advance Pricing Agreements of 14th November 2019.

The cooperation agreement is intended to ensure that a taxpayer complies with tax law while maintaining transparency in their activities and mutual trust and understanding between the tax authorities and the taxpayer, taking into account the nature of the taxpayer’s business.

The agreement may be concluded by taxpayers with revenues of at least 50 million EUR. The main benefits of the agreement are:

Exemption from reporting of national tax schemes (MDRs)

A 50% reduction of the fee for submitting an APA application

Attributing good faith to the taxpayer.

The taxpayer, being a party to the cooperation agreement, has the opportunity to discuss (with the Head of the National Revenue Administration) important issues related to the tax settlements, such as:

Interpretations of tax law

Determinants of transfer pricing

Non-applicability of the general anti-avoidance rule

The amount of advance income tax

Other, necessary to ensure the proper implementation of the cooperation agreement.

Penalties

At present, the sanctions for the use of non-market prices for transfer pricing in Poland are as follows:

10% (basic rate) of the sum of the undue or overstated tax loss and not reported (in whole or in part) taxable income to the extent resulting from this decision

20% (increased rate):

if the basis for determining the additional liability is exceeding 15 000 000 PLN

in the case of failure to submit transfer pricing documentation

30% (increased rate): the cumulative fulfilment of both conditions above

Furthermore, the Fiscal Penal Code provides a fine up to 720 daily rates per day in the following situations:

late submission, factually incorrect or failure to submit a statement that the Transfer Pricing documentation has been prepared. Late submission, factually incorrect or failure to submit TP-R information.

On the other hand, 240 daily rates per day are provided in the following situations:

preparation of transfer pricing documentation after the deadline

late submission of the TP-R information.

Affecting both domestic and foreign businesses, a number of actions triggers the obligation to register for Value-added tax in Poland. To provide a basic overview, our Polish experts prepared a comprehensive eBook on value-added tax. Find out more about VAT rates, registration of taxable persons, communication with local tax authorities, compliance and VAT return filing, VAT refund to EU member states or third countries and penalties.

The basic VAT rate in Poland is 23%. Reduced VAT rates of 0%, 5% and 8% apply to a wide range of goods which may change over time (special decree is issued in this respect). In general, lower rates apply to specific hygiene products, books, newspapers and food products. Each product or service should be considered individually.

Export within and outside the European Union

Intra-community supplies of goods and exports outside the EU are under several conditions subject to exemption with deductibility right (0% tax rate is applied).

Taxable amount

The taxable amount is understood as any kind of remuneration received or due in exchange for the supply of goods or provision of service. The tax base also includes other additional payments of similar nature, which have a direct impact on the price of goods or services supplied by the taxpayer.

VAT registration of domestic taxable persons

Voluntary and obligatory registration

In Poland, voluntary VAT registration is possible for entrepreneurs whose income in the last tax year did not exceed PLN 200 000. This VAT exemption is related to sales limit with some limitations for specific sectors. The possibility of voluntary registration is also available in selected cases whereas a VAT exemption rule is applicable.

The threshold for compulsory VAT registration is PLN 200 000 turnover. Entities exceeding this amount are obliged to register. Performing taxable transaction or exceeding the threshold triggers the registration duty which should be performed by filing specific form.

Group registration for taxable entities

From 1 January 2023, it is possible for related entities to settle VAT jointly through a VAT group.

A VAT Group is a group of financially, economically, and organizationally related entities. In simplified terms, entities belonging to a VAT Group are treated as a single VAT taxpayer.

Other specifications of the VAT registration

In Poland there are formal and material conditions stated in the VAT regulation, therefore even entities who do not have the status of VAT taxpayers formally can still be considered as entities performing activities subject to VAT.

If an entity intends to do business with foreign contractors from EU countries, they must register as a taxpayer of EU VAT. Although they are not obliged to register as an active VAT taxpayer, however, if they make an intra-community acquisition of goods (WNT) and the total value of these transactions exceeds PLN 50 000 during the tax year, they are obliged to account for VAT on these transactions (despite the fact that there is no obligation to settle VAT in respect of other business activities). The obligation to register for EU VAT (irrespective of the VAT exemption) also applies to:

The purchase of services from contracting parties in the EU for which the place of performance is in the purchaser’s country

Intra-community supply of services for which the place of taxation of the transaction is in the country of the person acquiring the goods.

If the entity is exempt from VAT and registers as a taxable person of EU VAT, they do not lose the right to be exempt from VAT.

VAT registration of foreign taxable persons

Definition of foreign taxable persons

In Poland, foreign entities are understood as legal persons, organisational entities without legal personality and natural persons with registered office or a fixed place of business outside the territory of Poland, carrying out activities which are subject to Polish VAT regulations.

Voluntary and obligatory registration for foreign taxable persons

Foreign entities may benefit from VAT exemption (under the SME procedure) if the following conditions are jointly met:

annual turnover in the territory of the European Union in the previous and current year has not exceeded the amount of EUR 100,000,

the value of sales in Poland in the previous and current year has not exceeded the amount of PLN 200,000 (in the case of commencement of sales in Poland during the year, this limit is calculated in proportion to the period of sale in the tax year),

do not perform in Poland any activities that exclude exemption from VAT (analogous to domestic entities).

For distance sellers from the EU, who are selling the goods to customers in Poland, the VAT registration threshold (for Intra-Community Distance Sales of goods) is PLN 42,000.

Communication with authorities

Local statutory representation for VAT

Representation of the taxable person in front of the Polish tax authority by a tax advisor is not obligatory. The obligation of representation occurs when the taxable person does not have a registered office or a fixed establishment in the territory of an EU Member State.

Statutory language

In communication with the tax authorities, only Polish language may be used.

Communication with authorities

A taxpayer may communicate with the tax authorities both electronically and by post. However, the VAT returns must be submitted electronically.

Companies in Poland are obliged to submit the JPK_VAT files containing both the VAT returns and the Standard Audit File (SAF), while the VAT records must be kept in an electronic system.

VAT compliance and return filing

Tax period and deadline for JPK_VAT (SAF-T) filing

The tax period equals the respective month, or the calendar quarter (only for small taxpayers registered for more than 12 months as active VAT taxpayers, with some exceptions).

In Poland, there is no “traditional” VAT return, but there is a requirement to file a JPK_VAT (SAF-T) covering both the declaration part and the recording part of VAT settlements. The deadline for filing JPK_VAT (SAF-T) is the 25th day after the end of a settlement period. Taxpayers settling VAT quarterly submit monthly (to 25th day after the end of month) the recording part of JPK_VAT (SAF-T) and on the 25th day of each month following the quarter submit the recording and declarative part of JPK_VAT (SAF-T).

Upon the demand of the authorities, the following electronic documents should be submitted:

Accounting books (JPK_KR)

Bank statement (JPK_WB)

Magazine (JPK_MAG)

VAT invoice (JPK_FA)

Tax revenue and expense ledger (JPK_PKPIR)

Income records (JPK_EWP).

EC sales list and other documents

EC sales list (or the so-called VAT_UE return) should be submitted electronically by the 25th day of the month for the previous month – the same time as in case of the JPK_VAT (SAF-T).

VAT refund to EU member states

Minimum amount and applicable period

In order to file for refund, the value of VAT may not be less than the PLN equivalent of the following amounts:

EUR 400 – in case the period (for which a refund request is filed) is shorter than the tax year, but exceeds 3 months

EUR 50 – in case the period (for which a refund request is filed) concerns the whole tax year or a period shorter than the last 3 months of the year

The conversion of the amounts mentioned above expressed in EUR shall be carried out according to the average exchange rate of the euro announced by the National Bank of Poland, in force on the last business day preceding the date of issue of the invoice or customs document.

The amounts used to determine the tax base determined in a foreign currency may be converted by a taxpayer into PLN in accordance with the rules for conversion of income determined in a foreign currency resulting from the income tax regulations applicable to that taxpayer for the purpose of settling a given transaction.

Given entity may apply for a tax refund for a period exceeding 3 months and not longer than 1 tax year, or for a period shorter than the last 3 months of the year. The requested amounts of tax in the given period is established based on the invoices documenting the acquisition of goods and services or based on the customs clearance documents in case of import.

Deadline and place of filing for VAT refund

The deadline for filing a VAT refund request falls on September 30th of year following the year covered by the request. It should be submitted in Polish to the tax administration in electronic form.

The deadline for tax refund falls on the 4th month after the request for refund is filed, including all supportive documents. The tax office will refund the indicated amount of tax no later than within 10 working days from the day of taking a decision on the amount to be refunded.

Refund for foreign taxable persons

Upon the fulfilment of specific conditions VAT refund for a foreign taxable person is possible.

VAT refund to third countries

VAT refund conditions

VAT refund to third countries is possible, upon the fulfilment of specific conditions.

Minimum amount and applicable period for VAT refund

In case of VAT refunds to third countries, the same rules apply as in case of VAT refund to EU member states (see VAT refund to EU member states – Minimum amount and applicable period for more information)..

Deadline and place of filing for VAT refund

The deadline for filing a VAT refund request in case of refunds to third countries is the same as in the case of EU member states, i.e., it falls on September 30 of next year and must be submitted electronically in Polish language. The deadline for VAT return also falls on the 4th month after the request for refund is filed, while the tax office conducts the refund also within the 10 working days after taking a decision on the amount to be refunded.

Special VAT regulations

White List

For VAT settlements, the White List is of great importance. It is a generally available register of VAT taxpayers where registration and bank account must be verified before an invoice is settled.

Payment to an account outside the White List in certain cases involves joint and several liability and the exclusion of the expense from the tax-deductible costs for income tax purposes.

Split payment

Split payment is a payment mechanism under which payment for goods or service is made by the purchaser to the supplier’s bank account and:

The net sale amount is credited to the supplier’s basic settlement account

The VAT amount is paid to a dedicated VAT account that it automatically created by the bank as an additional account to every business/trading settlement account.

In principle, the use of split payments is voluntary and depends on the purchaser’s decision to apply it. However, in the case of making payments for goods or services listed in Appendix 15 to the VAT Act, documented with an invoice in which the total amount due exceeds the amount of PLN 15,000, purchasers are obliged to apply the split payment.

National System of e-Invoices (KSeF)

From January 1, 2022, taxpayers can use the National e-Invoices System (KSeF). KSeF is a system that enables the issuing and sharing of structured invoices. The system is currently voluntary. The mandatory National e-Invoice System will come into force on 1 February 2026 for entrepreneurs with sales in excess of PLN 200 million, and from 1 April 2026 for all entrepreneurs.

Taxpayers will not be obliged to issue electronic invoices in KSeF in 2025. KSeF remains a voluntary solution at this point. KSeF will be obligatory for domestic entities and all taxpayers with a registered office or permanent place of business in the country.

Penalties for VAT non-compliance

Depending on the situation, the VAT sanctions amount to:

up to 100%

The highest penalty rate in VAT is when a tax person knowingly participates in tax fraud by deducting VAT from the invoice:

issued by a non-existent entity,

stating activities that have not been performed, in the part concerning these activities,

providing amounts inconsistent with reality, in the part concerning these items,

confirming the activities to which the provisions of Art. 58 and Art. 83 of the Civil Code (Journal of Laws of 2020, item 1740, as amended) – in the part relating to these activities.

up to 30%

This applies when the submitted VAT return has indicated:

the amount of the tax liability is lower than the amount due

the amount of the refund of the tax difference or the amount of the input tax refund higher than the amount due

the amount of the tax difference to reduce the amount of tax due for the next settlement periods higher than the amount due

the amount of the refund of the tax difference, the amount of the input tax refund or the amount of the tax difference to reduce the amount of tax due for the next settlement periods, instead of showing the amount of the tax liability to be paid to the tax office.

This sanction also occurs in the case of non-filing of the tax return and non-payment of the tax liability amount.

20%

The penalty applies if, after the tax audit or customs and tax audit, the taxable person submitted:

VAT return adjustment taking into account the identified irregularities and paid the amount of the tax liability or returned the undue amount of the refund no later than on the date of submission of this correction

VAT return and paid the amount of the tax liability on the date of submission of

the declaration at the latest

, after the tax audit or customs and tax audit, the taxable person submitted:

15%

If the taxable person submitted the VAT return adjustment and paid the amount of the tax liability returned the undue amount of the refund no later than on the date of submission of the VAT return adjustment.

Apart from sanctions under the VAT Act, there are also sanctions in the Fiscal Penal Code that should be taken into consideration.

Get expert support for value-added tax in Poland

Dealing with value-added tax in Poland can be complex, especially with frequent legislative updates and detailed reporting obligations. Accace offers comprehensive VAT services in Poland to help you manage VAT registrations, filings, audits, and day-to-day compliance with ease. Our local experts ensure your obligations are met accurately and on time, so you can focus on growing your business with confidence.

Employing expatriates in Poland or posting employees abroad brings a new set of obligations to any employer. Our Polish tax and labour law experts gathered all the crucial information related to cross-border employment for fiscal compliance, to provide you with a basic knowledge on the topic. Get an easy overview on expat tax in Poland, such as conditions for tax residency, personal income tax, social security and health insurance contributions or penalties for non-compliance.

Overview of key facts related to expat tax in Poland

Our local tax, payroll and labour law experts are here to help you – as an expat or an employer – to obtain essential expert advice, so that you can effectively address all the matters related to cross-border mobility in Poland and other locations globally.

Tax residency

In Poland, tax residents are natural persons, who:

Have a centre of personal or economic interests (centre of vital interests) on the territory of Poland

They stay on Polish territory for more than 183 days in a tax year

Tax rate

Tax rate on income up to PLN 120,000

12%

%

Tax rate on income exceeding PLN 120,000

32%

%

Tax period

Calendar year

Social security contributions

Rate for the employer

20.48%

%

Rate for the employee

13.71%

%

Health insurance contributions

Rate

9%

%