Get free access to

Our legislation updates make it easy for you to keep on top of the latest changes affecting your business. Receive our articles, opinions, tips, industry news, country profiles, regional overviews and studies, latest events and even more, directly into your mailbox.

Check out our Newsroom to see what is included!

We will send you only relevant information we consider may be of your interest and treat your personal data in compliance with our Privacy policy and GDPR statement.

Unable to subscribe? Try this page.

IFRS Foundation published educational material to support companies in applying going concern requirements. In current pandemic, many entities face falling revenues and decline in their profitability and liquidity which raise the question about their ability to continue as going concern. Therefore, management needs to involve a greater deal of judgement as in preceding period that should be disclosed. Those disclosures are likely to be more relevant for users of financial statements, too.

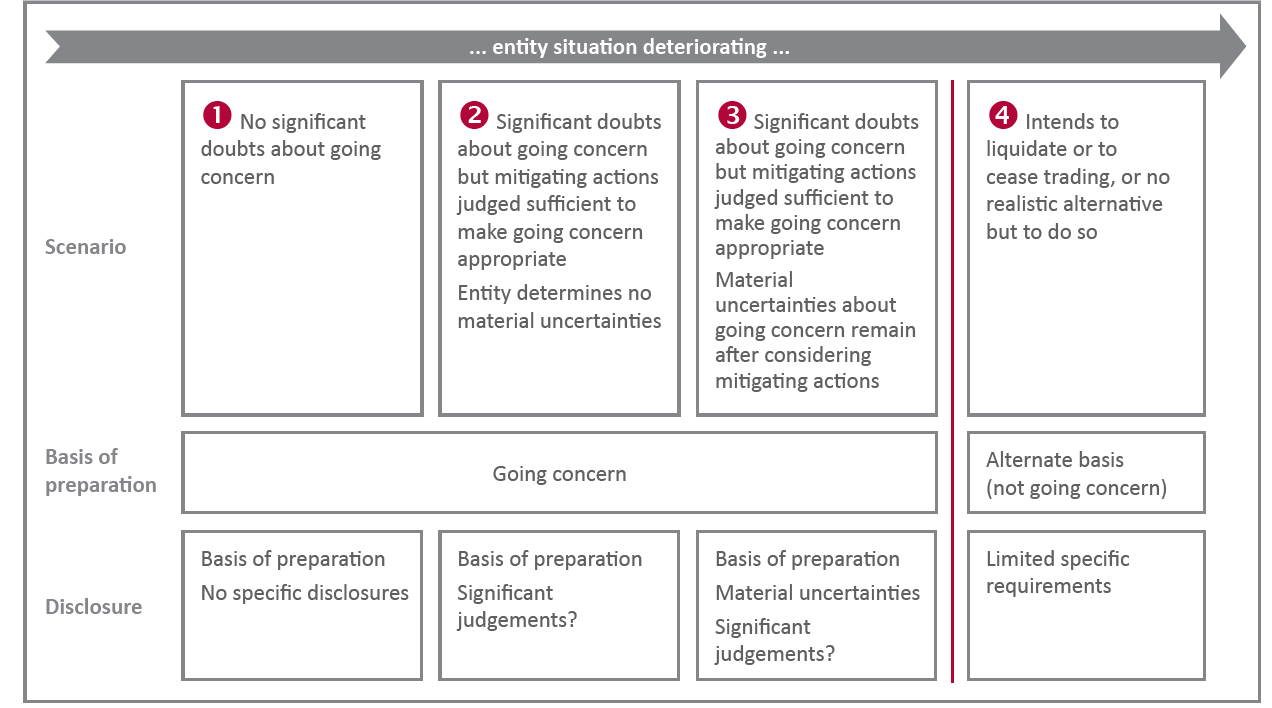

IAS 1 stands that “An entity shall prepare financial statements on a going concern basis unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so.“ Assessment is made for 12 months at least and includes:

Entity should also disclose any change in ability to continue as going concern in accordance with IAS 10 Events after the Reporting Period. If, before the financial statements are authorised for issue, circumstances were to deteriorate so that management no longer has any realistic alternative but to cease trading, the financial statements must not be prepared on a going concern basis.

Possible situations when applying the requirements

The requirements in IAS 1 can be depicted as set out in diagram below*:

*IFRS Foundation – Going concern – a focus on disclosures, January 2021

About Accace

Accace is a proactive consultancy and outsourcing partner who bridges the gap between needs and solutions. Combining smart and streamlined technology with a holistic approach, we provide an all-round care to clients and consider their matters as our own. With over 800 experts and approximately 2,000 customers, we have vast experience with facilitating the smooth operation and growth of small to large-scale, global businesses.

About Accace Circle

Accace operates internationally as Accace Circle, a co-created business community of like-minded BPO providers and advisors who deliver outstanding services with elevated customer experience and erase the borders of service delivery. Covering over 60 jurisdictions with more than 7,000 professionals, we support over 80,000 customers, mostly mid-size and international Fortune 500 companies from various sectors, and process at least 800,000 pay slips globally.